29 October, Kathmandu. According to the goal taken by the Government of Nepal within the present monetary yr (FY) 2079/80, it’s seen that there will likely be an absence of assets to gather the nationwide debt (inner debt). For this, there’s a chance that the banks must present loans to the federal government in settlement with Nepal Rastra Bank.

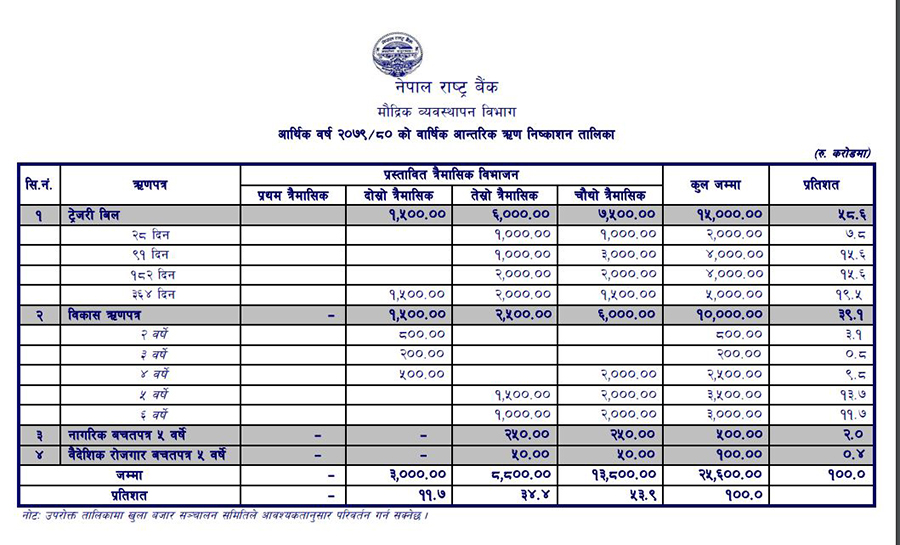

The authorities of Nepal has set a goal of managing assets of two trillion 56 billion from inner debt with a purpose to fulfill the aims set within the funds of the present fiscal yr 2079/80. According to this, Nepal Rastra Bank has already printed the (inner debt) assortment schedule.

According to the nationwide debt assortment desk printed by the Central Bank, the goal is to gather 6 billion rupees out of 256 billion rupees by international employment financial savings bonds and citizen financial savings bonds. The goal is to lift the remaining 250 billion nationwide debt by treasury payments and improvement bonds.

According to former banker Bhuvan Dahal, the primary a part of the funding in inner debt, which goals to be raised by improvement bonds and treasury payments, is the share of banks and monetary establishments.

According to the info of the Ministry of Finance as of the tip of June 2079, the whole inner debt of the federal government is 9 trillion 86 billion 11 billion. Of which the funding of banks and monetary establishments alone is 9 trillion 9 billion 78. This exhibits that the share of funding of banks and monetary establishments within the inner debt of the federal government is greater than 90 p.c.

57 billion to handle liquidity

According to the info of Nepal Rastra Bank on November 28, the excellent stability taken by the banks to handle liquidity is about 57.78 billion. Since the start of the present monetary yr, Nepal Rastra Bank has despatched liquidity to the system by outright buy of 72 billion 20 million treasury payments to handle the dearth of liquidity with the banks.

Even if the banks are to depart the remaining 58 billion in liquidity to the Rashtra Bank as it’s now, 2 and a half billion assets should be managed to lift home debt as per the federal government’s goal within the subsequent 8 months. The foremost supply of which is the deposits of banks and monetary establishments.

According to the info of Nepal Rastra Bank dated November 27, the common credit score to deposit ratio (CD ratio) of banks and monetary establishments is 87.12 p.c. According to the principles and rules of the National Bank, the CD ratio could be elevated to a most of 90 p.c.

According to the present CD ratio, if the banks lengthen the mortgage by 1 p.c, the brand new mortgage will likely be greater than 50 billion. In that case, the quantity that the banks must take from the Rashtra Bank for liquidity administration will exceed 1 trillion. The foremost financial instrument utilized by banks for liquidity administration is Permanent Liquidity Facility (SLF).

Nepal Rastra Bank has introduced that by the financial coverage of the present monetary yr, Nepal Rastra Bank will tighten the SLF facility. However, it has not been carried out. At current, banks have been taking the required SLF facility based on the collateral capability of presidency financial savings bonds.

However, now the National Bank is attempting to rearrange that SLF can’t be taken a couple of p.c of the home deposits of the banks.

Banks and monetary establishments will likely be offered everlasting liquidity services on the financial institution charge for a most interval of 5 days for the collateral of the bonds specified by this financial institution, offered that the excellent stability of the whole deposits within the home foreign money of the respective establishments on the finish of the earlier week will not be greater than 1 p.c. This association will likely be carried out by making vital amendments within the current process,’ the financial coverage says.

On this foundation, the banks which might be at present taking SLF services will now be strict in such services. However, it’s talked about within the financial coverage that the final creditor facility could be taken by the banks at 2 p.c penal curiosity on the financial institution charge.

Banks and monetary establishments which might be unable to handle the required liquidity by the interbank market, every day liquidity services, open market transactions and everlasting liquidity services will likely be supplied with a penalty charge of two share factors on the financial institution charge if requested by the establishment. It has been stated.

Banker Bhuvan Dahal says that based on the present system, banks are investing in authorities bonds by taking a contract with the federal government and that apply is incorrect. He argues that banks ought to make investments provided that they’ve the capability to take action, and in the event that they pledge authorities financial savings bonds and take collateral from the National Bank after which spend money on authorities bonds, it is going to trigger one other downside.

Officials of Nepal Rastra Bank additionally say that because of the present challenges within the exterior sector, there’s a have to rethink even the assure of presidency financial savings bonds. Now authorities financial savings bonds are additionally being utilized in money circulation.

However, an official of Nepal Rastra Bank stated that because of the present issues within the exterior sector, money move must be achieved solely with 100% international foreign money as collateral.

‘Government Savings Paper is the federal government’s capability to borrow as a lot because it wants, when money move relies on the truth that it is going to result in one other disaster within the financial system. Now now we have to suppose in that route as effectively’ says an official of Nepal Rastra Bank.

At the tip of final June, the quantity of presidency bonds taken as collateral by the banks reached about 2.5 trillion. The quantity which the banks have invested within the authorities financial savings bonds by maintaining the federal government bonds as collateral.

Although the banks take extreme deposits to handle liquidity and the short-term rates of interest are additionally excessive, Bima Rastra Bank has lowered the banks’ funding in authorities bonds by instantly buying about 73 billion treasury payments. In the identical method, the federal government has additionally paid some loans, whereas the National Bank has bought treasury payments value about 50 billion rupees whereas speaking about renewing them. Which has lowered the amount of cash taken by the banks with the National Bank. Which can be the objective taken by the National Bank by financial coverage. A senior official of the nation stated that the explanation for the strict coverage of the National Bank within the present financial coverage is to make sure that the federal government financial savings bonds aren’t re-invested within the authorities financial savings bonds.

Banker Bhuvan Dahal says that banks have taken SLF and invested in authorities loans, and Rashtra Bank ought to examine it. “It is a giant downside to spend money on authorities bonds after taking authorities bonds and financial savings bonds as collateral,” says Baiker Dahal. Banks do not give cash they do not have.’

Banker Bhuvan Dahal says that banks have taken SLF and invested in authorities loans, and Rashtra Bank ought to examine it. “It is a giant downside to spend money on authorities bonds after taking authorities bonds and financial savings bonds as collateral,” says Baiker Dahal. Banks do not give cash they do not have.’

According to banker Dahal, provided that the inner debt is to be raised based on the goal set by the federal government, 2.5 billion assets are wanted. He argues that because of the demand for loans, extra assets will likely be wanted to increase.

He argues that as an alternative choice to resolve this, the federal government can take loans instantly from the residents by rising the rate of interest of improvement bonds, however that can result in the problem of managing the CD ratio once more as the cash will exit from the banks.

Banker Dahal stated, “The inner assets at present being collected within the financial institution aren’t sufficient to lift inner debt based on the goal set by the federal government and provides loans based on the demand of the personal sector,” banker Dahal stated. It is unlucky that the federal government has to borrow from the federal government bonds by subpoenaing the banks.’